Import dependency on China continues to grow

For some years now, a debate has been sparked in Germany about the resilience of supply chains and dependencies on individual states. In 2022, this debate was largely driven by the Russian war of aggression on Ukraine, which unsparingly demonstrated the negative consequences of dependence on Russian oil and gas for the German economy. Before the war, dependence on China in particular was considered problematic, and the war has also put this in a new light. In particular, China's geopolitical aspirations with regard to Taiwan are seen as threatening. This figure of the month therefore looks at bilateral trade between Germany and China.

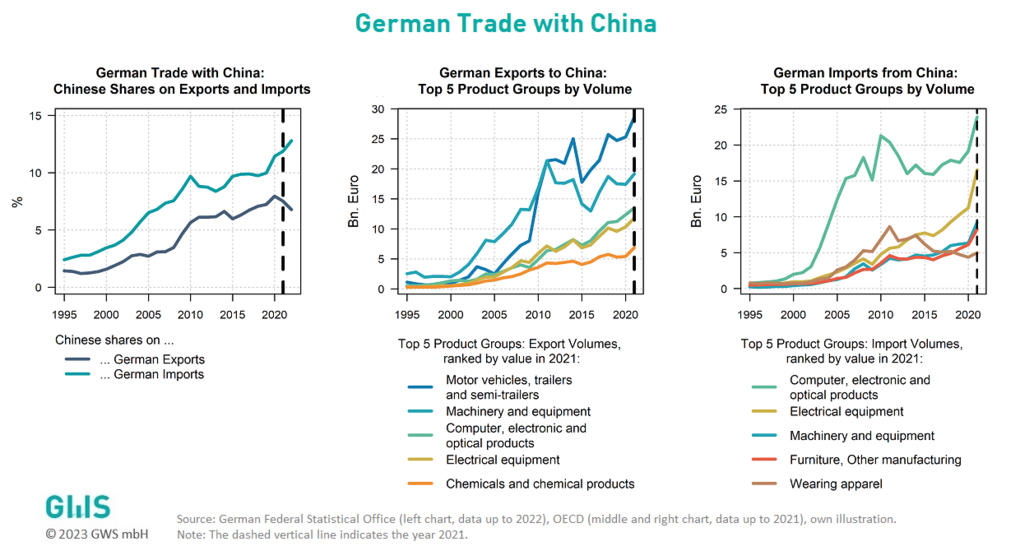

In the chart on the left, one can see the progression of the Chinese share of German exports and imports since 1995. Both shares have been steadily increasing. Interestingly, despite the debate over Germany's dependence on China during this period, the import share jumped in 2020: From 10% in 2020 to just under 13% in 2022. The Chinese share of German exports, on the other hand, has fallen during this period and is around 7% in 2022.

The graphs in the middle and on the right provide information on the respective 5 product groups, with the highest export volume to China, and the highest import volume from China, respectively. The top 5 export product groups include the typical German industrial and export hits. The top 5 product groups on the import side are partly the classic labor-intensive goods of the clothing and furniture and other manufacturing industries, but also goods of the highly specialized machinery-intensive industry. The high level of imports from the product groups of computers, electronic and optical products, and electrical equipment reflects the high demand from German industry for highly specialized preliminary and end products such as chips or solar equipment.

In terms of Germany's dependence on China, it can be concluded from the three charts that German dependence on China has increased significantly in recent years, and in particular has increased significantly again since 2020. The manufacturing sector, in particular, is dependent on China due to the import of intermediate inputs from China and the purchase of end products. The trend in the data suggests that this dependence is likely to increase further.

Other figures can be found here.